This is the sixth installment of our interview series “Where is the General Theory of the 21st Century?”

Blanchard on DSGE and the State of Macroeconomics | #WITGT21 Conversation Series | EconReporter

Continuing our previous discussion on “DSGE model and the State of Macroeconomics”, Professor Olivier Blanchard further explained the role empirical research on DSGE models, how to teach undergraduates macro after the Great Recession, and his research on hysteresis.

(The transcript below has been edited for length and clarity. All mistakes and miscommunications are ours.)

Q: EconReporter B: Olivier Blanchard

Q: What is the role of empirical work in the development of DSGE models? Is it possible to have a bigger role for empirical models to be in the DSGE model?

B: The current approach is to use calibration rather than estimation for most of the coefficients. Then, to do Bayesian estimation to estimate the remaining parameters and the system as a whole.

I think the evidence from the vast body of econometric work should be used much more. To specify the consumption function, we should do it using all kinds of information, single equation estimation, natural experiments, case studies or anything else. And to use all these pieces to characterize a consumption function which can then be put in the DSGE model.

Once this is done, we want to make sure that the DSGE replicates the VAR representation of the data. If the dynamics of the DSGE are close to those of the VAR, the job is done. If not, one has to go back to the drawing board, and see why the DSGE model is not replicating the VAR dynamics.

But this is a completely different exercise, which involves building on the work of hundreds of people who do partial equilibrium estimation. This is not done at this point, and DSGEs are largely operating within an intellectual silo, with not enough interaction with the rest of the empirical work going on in macro.

Q: Is the way to build a model you have just mentioned too ideal to be possible? Or is it just macroeconomists not working fast enough to make significant progress in macroeconomics?

B: I think that there is a lot of progress. If you look at, say, the NBER working papers, there are five or six macroeconomics papers coming out every week. They are all extremely interesting.

What happens is that these research have not been fed into the DSGE models. The DSGE models live in their own universe. They do not build enough on the very good work that is happening in macroeconomics in the recent years.

So it is not that we don’t have enough good research. It is that there are not enough coordination and integration of the results.

Q: Is there any other ways to speed up the progress in coordinating and integrating the research? Maybe the IMF Annual Research Conference “Macroeconomics after the Great Recession” you co-hosted this year is one of those efforts to further the coordination?

Q: In another one of your note “How to teach intermediate Marco after the crisis”, you have mentioned a IS-LM-Phillips Curve model. Is this a kind of toy model you have just mentioned? Are you confident that more students will learn about this?

B: Actually, I have done just that in my own textbook.

If I have to teach undergrad, I don’t want to teach 200 models, right? The students are not ready to use Matlab or any complicated programming, so we cannot teach the DSGEs. But we must teach toy models.

If I have to teach undergrads, or to explain something to my mother or to my friends, I think using an ISLM with two interest rates plus a Phillips Curve, is the best way to talk about most of the issues that are relevant today.

B: Yes, It’s different. As you may know that the 5th edition was published before the crisis, and the 7th edition is published this year, so there are several major changes.

The first change between them is that I have introduced a financial sector in the basic model. Traditionally, the ISLM only has one interest rate, which is the rate set by the central bank. It is the same rate in the LM and the IS curve. That’s clearly not right. A lot of what happened in the financial crisis is that even if the central bank lowered the policy rate, the rate relevant to investment decisions turned out to be a very different and much higher rate.

So, I think it is very important to have two rates, one determined by the central bank, and another which is relevant for people and firms when they borrow. This is a way to introduce the financial system. If the financial system is in good shape, the two rates tend to be close; if it is not, the two rates can be quite different.

The second change is in the LM curve. The old LM curve was derived on the assumption that the central bank chooses M, the money supply, and then the interest rate is determined by the market. It is clearly not true. Nowadays, the central banks choose the rate. So, that’s how we should think about the LM curve, which is at the rate chosen by the central bank.

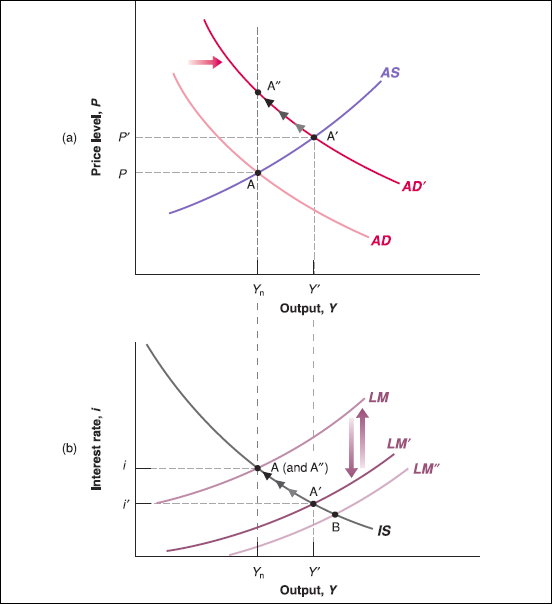

The third change is that I have given up on Aggregate Supply and Demand model (ASAD). It is because, firstly, ASAD was quite complicated. It is not great from the point of view of being a toy model. But also, ASAD is misleading as it has the very strong message that even if no economic policy is implemented, the economy will return to the equilibrium all by itself.

As I have written in the 5th edition, if there was an adverse shock in the ASAD model, the price level would decrease, then real money supply would increase, this lowered the interest rate, which would have pushed the economy right back to its potential output level. (The figure below is an illustration of a reserved example which start with a positive shock on demand. The figure is from “Macroeconomics:A European perspective” by Olivier Blanchard, Alessia Amighini, Francesco Giavazzi.)

This mechanism is more or less irrelevant now. Economies do not return to health all by themselves, central banks do not keep the nominal money supply constant. So I gave up on AS, instead, I use the Phillips Curve as a description of the supply side. It gives a much more realistic description of what happens.

Q: In my previous interview , Professor John Cochrane mentioned that he thought that Fiscal Theory of Price Level (FTPL) may be the missing link of New Keynesian model. What do you think about the FTPL’s prospect in incorporating in mainstream models?

B: I don’t believe it.

It would take a long time to explain, but I don’t find FTPL to be an attractive theory of determination of the price level. I believe however that the issue of fiscal dominance of monetary policy is an important one. There are many countries where fiscal policy determines monetary policy. If the ministry of finance is very powerful, it can force the central bank to monetize their bonds.

But this is a very different story from John’s fiscal theory of the price level.

Q: Federal Reserve Chair Janet Yellen, in her recent speech “Macroeconomic Research After the Crisis” , suggested four research topics macro researchers should work on. One of which, the problem of hysteresis, is a research topic you have been working on in recent years.

B: For the moment, it is just a hypothesis. Therefore, I think the way policymaker should deal with it is to assume it’s true, say, with a probability of 20%, but not with 100% probability. And then decide what should the policy be. For the moment, that’s what they should do.

Explainer: What is Hysteresis? | EconReporter

In terms of research, I am actually doing more research on this topic. I think you look at topics like this, you look at the micro evidence. There is interesting work on how, for example, long-term unemployed people drops out of the labor force. There is also some very interesting research on what happens to research and developments during the recessions.

But I don’t think we will ever be sure. I hope that I can convince few more people that it is important. Maybe, I can get the 20% to become 50%, in a few years’ time.

Q: Why economists are so hard to convince that there is hysteresis? I think it is very intuitive to laymen to believe that unemployment has long-term effect on the economy.

B: Let’s say, for example, people commit suicide as the result of being unemployed, that’s hysteresis, right? And we know in fact some people commit suicide. So it is clearly that the case.

But the important question for macroeconomists is how quantitatively important that is. One suicide is one big individual tragedy. But if it is just one, it doesn’t matter from the macroeconomics point of view, right?

So, the important thing is to show how big the effect is. How reliable is it? What type is it? Is it the case that they only exist in recessions? Or they also exist in booms? Is it asymmetrical? All these are the things that we don’t know.