Last Updated:

DSGE stands for “dynamic stochastic general equilibrium,” it is a methodology for a wide range of macroeconomics models.

As Blanchard described in his note “Do DSGE Models Have a Future?” , DSGE Models have three major modeling characteristics.

As its name suggested, one important aspect of the DSGE models is its “dynamic” feature. “Dynamic” means that expectations of the future are a crucial determinant of today’s outcome, i.e. output and inflation tomorrow, and thus their expectations as of today, depend on monetary policy tomorrow, and whatever will happen from then into the infinite future.

Therefore, in the DSGE models, expectations are the main channel through which policy affects the economy.

One of the most common formulations is the so-called New Keynesian model. New Keynesian economics can be interpreted as an effort to combine the methodological tools developed by real business cycle theory with some of the central tenets of Keynesian economics tracing back to Keynes’ own General Theory. In the New Keynesian model there are several basic features:

First, the behavior of consumers, firms, and financial intermediaries, when present, is formally derived from microfoundations, i.e. they are normally based on microeconomics theories or empirical findings.

Second, the underlying economic assumption is that there is a competitive economy, but with a number of essential distortions added, e.g. nominal rigidities, monopoly power, or information problems.

Third, the model is estimated as a system, rather than equation by equation in the previous generations of macroeconomic models.

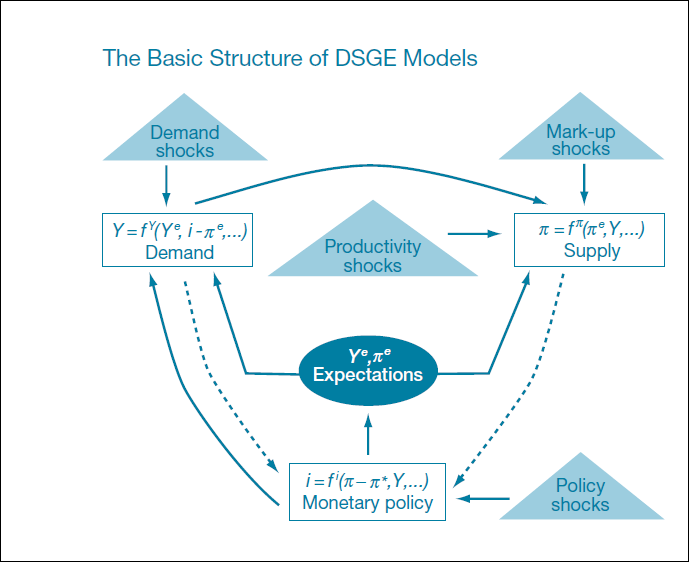

As Jordi Galí explamified in his paper “The State of New Keynesian Economics: A Partial Assessment,” the simplest form of New Keynesian DSGE model is the so-called three-equation model, which as the name suggested, composed of three relationships. First, the dynamic IS equation states that the current output gap is equal to the difference between the expected output gap one period in the future and an amount that is proportional to the gap between the real interest rate and the natural rate of interest.

Second, the New Keynesian Phillips curve, states that inflation depends on expected inflation one period ahead and the output gap. The third one is an interest rate rule, which describes how the nominal rate of interest is determined; in the most common settings, Taylor Rule, in which nominal interest rates traditionally rise and fall based on the current inflation rate and detrended output, is used as the interest rate rule.

And as explained in “Policy Analysis Using DSGE Models: An Introduction” by Sbordon, Tambalotti, Rao and Walsh, most of the DSGE models policy analysis are trying to explains how the three relationship reacts to certain kind of shocks, e.g. demand shock, productivity and other kinds of supply shock, and policy shock.

(Read the full interview: DSGE model and the State of Macroeconomics — Q&A with Olivier Blanchard)

(Read the full interview: DSGE model and the State of Macroeconomics — Q&A with Olivier Blanchard)