Ben Bernanke has a new blog post on Brookings. The focus of the post is to explain “the large difference between the reactions of the Fed and the markets to the change in fiscal prospects since the election”.

What is interesting to me is his view on the potential effect of the Trumpian expansionary fiscal policy. Here is one bit:

When I was Fed chair, I argued on a number of occasions against fiscal austerity (tax increases, spending cuts). The economy at the time was suffering from high unemployment, and with monetary policy operating close to its limits, I pushed (unsuccessfully) for fiscal policies to increase aggregate demand and job creation. Today, with the economy approaching full employment, the need for demand-side stimulus, while perhaps not entirely gone, is surely much less than it was three or four years ago.

This is very similar to what Paul Krugman keeps saying these days. For example, this one:

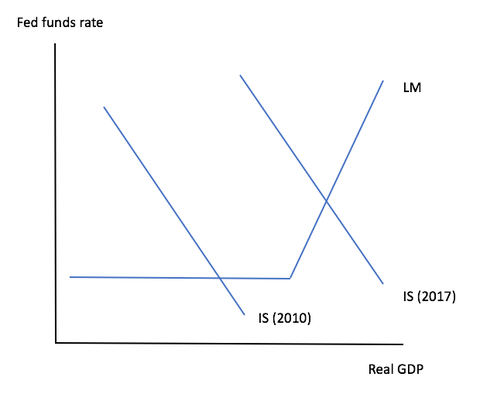

In the aftermath of the financial crisis, however, we spent an extended period at the ZLB, as shown by the “2010” IS curve. In those conditions, shifts in the IS curve don’t move interest rates, there is no crowding out (actually crowding in because increased sales lead to higher investment), and multipliers are large…

…are we still there? No. Wages are finally rising, quit rates are back to pre-crisis levels, so we seem to be fairly close to full employment, and the Fed is raising rates. So it now looks like the “2017” IS curve in the figure. We’re just barely over the border into normality, which is why I think the Fed should hold and we could still use some fiscal stimulus for insurance, and very low rates still make the case for lots of infrastructure spending. But it’s not the same as it was.

Later in the blog post, Bernanke tries to explain why the Fed might consider the effect of the fiscal policy would be small:

Based on what we’ve heard both from Trump and from congressional Republicans, personal tax cuts, especially for higher-income households, are likely to be a big part of the program, and probably the easiest part on which to reach agreement. However, whatever the longer-term benefits of tax reform, high-income consumers may save much of any tax cut they receive, implying that the effects on demand of such cuts are likely to be smaller than the effects of direct government spending.

The blog post has made other potential explanations on why the Fed haven’t changed the economic forecast in the light of the “bigly” fiscal stimulus, worth reading.

(Just don’t expect to see any mention of “Monetary Offset”, nor one should expect he will shout out loud “hike rate faster!”)

🙂

Read the Whole Thing: The Fed and fiscal policy | Brookings Institution

The Fed and fiscal policy | Brookings Institution

>>> You can follow EconReporter via Bluesky or Google News